|

Back to Blog

Read Peter Oakes's Media Contributions31/12/2026  February 20, 2025

The best board advice? Don't rush in February 6, 2025 Why the Guinane case is a game-changer for the C-suite Banking Risk & Regulation (Financial Times) December 5, 2024 Regtech Failures Plaguing European Banks ACAMS MoneyLaundering.com November 28, 2024 Central Bank warns some Irish fintechs still failing to fulfil ‘basic’ obligations Business Post March 03, 2024 How much is your confidential and personal data worth on the dark web worth? Peter Oakes November 05, 2023 Buckle up fintechs, it’s going to be a rough new EU rules order Irish Independent November 05, 2023 Credibility and jobs: Why Dublin wants to land the EU’s laundry basket Sunday Times February 03, 2023 In Malta, AML Failures Trigger Penalties Against Local Cryptocurrency Platforms ACAMS MoneyLaundering.com January 12, 2023 Jack Ma profile: how China is making the Alibaba and Ant Group founder pay for his outspoken stance Business Post January 10, 2023 Interview with Peter Oakes, Founder of Fintech Ireland Business Post / Wall Street Journal November 22, 2022 Louth MEP says tech job losses ‘shouldn’t be too much of concern’ as fintech future ‘looks bright’ Independent September 23, 2022 Is the party over? Irish tech braces for a shock as the easy money dries up Business Post September 15, 2022 What will happen to money in the United Kingdom? [Radio] Newstalk September 15, 2022 Financial Leadership Summit future-proofs CFOs Irish Times August 27, 2022 The Fintech 15: the people making waves in one of Ireland’s leading tech sectors Business Post June 17, 2022 Tide turns on crypto currencies as recession fears stalk markets Irish Times May 11, 2021 To Combat ‘Severe Consequences’ of De-risking, EU Wants Better Risk Assessments ACAMS MoneyLaundering.com April 10, 2022 ‘Defensive’ attitude of Central Bank putting off fintech investors Business Post March 30, 2022 Revolut rival Vivid withdraws application for Irish e-money licence Irish Times March 22, 2022 EU AML Supervisors Disregarding Risk-based Approach ACAMS MoneyLaundering.com February 24, 2022 Irish-based expats adviser Abbey Wealth changes hands in CEO-led buyout Irish Times December 9, 2021 Increasing competition in the digital payments market RTE July 13, 2021 Banks Small in Stature, High in Risk Could Escape Direct EU Oversight ACAMS MoneyLaundering.com June 11, 2021 Ireland’s new biggest bank: How Barclays rose to the top Irish Times March 21, 2022 Winklevoss twins secure Irish e-money licence for Gemini Payments Irish Times October 22, 2020 Leveris Core Interview with Peter Oakes, Founder and FinTech Mentor at FinTech Ireland (Thought Leadership) Irish Tech News October 14, 2020 An Abundance of Financial Innovation (Thought Leadership) Soldo September 25, 2020 FinCEN Files: Scale of challenge facing financial regulators revealed in leaked documents Irish Times September 3, 2020 Banks Should Review Client Onboarded Remotely During Pandemic: Moneyval ACAMS MoneyLaundering.com June 11, 2020 The Irish Fintech Ecosystem: Headwinds and Tailwinds & the Making of a Global Fintech Centre (Thought Leadership) CPA Ireland Journal April 22, 2020 How to operate as a non-executive director of regulated firms [Podcast] Captivated Audience Podcast February 14, 2020 European Supervisors Instructed to Challenge Banks More Frequently ACAMS MoneyLaundering.com December 5, 2019 EU inches towards uniform AML rules and supervision ACAMS MoneyLaundering.com September 24, 2018 Ireland at the crossroads as prosperity and Brexit approach Australian Financial Review September 14, 2019 Bank to the future online banking set for big changes RTE September 12, 2018 EU Officials Pitch Expanded AML Oversight Role for European Banking Authority ACAMS MoneyLaundering.com August 31, 2018 The future of cash RTE June 17, 2019 Brexit: Bane of Banks and Bank Regulators alike ACAMS MoneyLaundering.com April 26, 2018 GDPR: where does it sit in the cyber security mix? Irish Times April 26, 2018 Cashing in on digital ‘wallets’ Irish Times March 11, 2018 Roubles rumbled: What we don't know about Russian money in the IFSC Irish Times January 28, 2018 Your Business: The future of money. It’s official: cash is no longer king Business Post January 9, 2018 Irish Regulator Proposes Holding Bank Managers Liable for AML Lapses ACAMS MoneyLaundering.com October 15, 2017 Beware Bitcoin Funding-Investment Mania Investors Told Independent.ie October 11, 2017 Small companies cheer sought after tax cut Independent August 13, 2017 Former Central Bank director and lawyer join Corlytics board Business Post July 23, 2017 Australia’s Ignition to open in Dublin - appoints Peter Oakes to advise on raising an additional €2 million Business Post June 07, 2017 Fintech Ireland event at the NCI to highlight work of Ireland’s financial innovators Business & Finance June 06, 2017 Peter Oakes joins the Advisory Committee of Kyckr (Global KYC Experts to Promote and Advise Kyckr) ASX May 21, 2017 Fintech fliers - Former Central Banker Peter Oakes and software engineering manager Dave Anderson of Fintech Ireland pick ten of the up-and-coming businesses to watch out for Business Post April 30, 2017 Money laundering: was AIB’s fine too low? AIB’s €2.275 million fine raises questions about Ireland’s laws – and the Central Bank’s enforcement approach Business Post March 20, 2017 Brexit & Regulatory Arbitrage and the fintech opportunities for Ireland [Radio] Newstalk February 5, 2017 Trump v Ireland Inc: How "America First" is being felt in Ireland Business Post February 5, 2017 Former central banker warns of danger in US regulatory rollbacks. Peter Oakes has said Irish banking needs to exercise caution after Trump's Dodd-Frank comments Business Post January 5, 2017 Why 2017 could be the year the 'robo-advisors' finally come to town Fora October 16, 2016 Vast slew of public settlements now due. The Central Bank could ramp up enforcement cases before the end of the year (Thought Leadership) Business Post October 4, 2016 Former Central Bank enforcement director in private sector move. TransferMate appoints Peter Oakes to board Business Post July 28, 2016 CEO Q&A: Peter Oakes on Challenges & Opportunities for Ireland’s fintech Industry (Thought Leadership) Business & Finance July 14, 2016 Fintech has a place within financial service ecosystem Irish Times July 13, 2016 No company is immune from data security threat Irish Times July 13, 2016 The CEO Interview, Peter Oakes, Founder of Fintech Ireland - Business & Finance (Thought Leadership) Business & Finance July 5, 2016 Powering forward: Peter Oakes discusses the prospects for Ireland’s fast growth fintech industry (Thought Leadership) Business & Finance July 3, 2016 Brexit: Leave result has thrown Britain’s financial world into a tailspin Business Post July 3, 2016 Summit looks at all aspects of Internet of Things Business Post June 26, 2016 Ireland falls short in enforcing money‐ laundering laws Independent June 7, 2016 Announcement of the Fintech20 Ireland Irish Tech News June 7, 2016 Fintech Ireland event at the NCI to highlight work of Ireland’s financial innovators Business & Finance June 1, 2016 Powering forward - growth prospects for innovative disrupters (Thought Leadership) Business & Finance May 19, 2016 Viewpoint The Variable Mortgage Rates Bill (Thought Leadership) Finance Dublin April 26, 2016 FBFSS Summit: Trust is the key to a digital future - In just 10 years we could be buying driverless car insurance from Google Business Post April 24, 2016 Fintech: More than Just a Marriage of Finance and Technology (Irish Times/Grant Thornton) (Thought Leadership) Irish Times (#GTech) March 13, 2016 Central Bank fires warning shot across stockbrokers’ bows. Concerns include personal account dealing, gifts and entertainment, and intragroup relationships Business Post January 31, 2016 Irish fintech sector is banking on boom Independent January 31, 2016 Has the Central Bank’s do-nothing culture changed? It's tough to find an answer to the question: What have we learned? Business Post January 01, 2016 Irish Australian Chamber of Commerce launches Irish chapter RTE May 31, 2015 Oakes heads for high frequency trader Business Post May 28, 2015 Presentation on Fintech to Financial Services Ireland (Thought Leadership) Financial Services Ireland April 22, 2015 Ireland plays for high stakes in fintech game Business Post April 22, 2015 Central Bank: Behind closed doors Business Post March 3, 2015 Presentation - Big Opportunities in Fintech (Thought Leadership) UK Trade & Investment October 7, 2014 Restrictions on the loan to value and loan to income ratios for house purchase [Radio] Part 1 / Part 2 NewsTalk with Ivan Yates September 13, 2014 The Future of Money [Radio] RTE August 8, 2014 Mortgages – Consumer Protection and Prudential debate [Radio] Part 1 / Part 2 NewsTalk with Ivan Yates July 6, 2014 Any debt deal will cover just 8pc of our €64bn loan Independent July 5, 2014 IMF & EU debt deal for Ireland [Radio] Part 1 / Part 2 / Part 3 RTE with Claire Byrne July 4, 2014 Digital currencies and other regulatory issues [Radio] Newstalk with Ian Guider January 9, 2013 The Enforcement Directorate at the Central Bank under Peter Oakes (Ian Guider and Jon Ihle) [Radio] Newstalk April 9, 2013 COMMENT: Elderfield's departure no surprise Business Post January 13, 2013 Market Week – Oakes Leaving Central Bank Business Post January 8, 2013 Oakes to step down from Central Bank Business Post January 8, 2013 Central Bank's director of enforcement to step down RTE December 11, 2012 Address by Director of Enforcement, Peter Oakes to Central Bank Enforcement Conference Speech (Thought Leadership) Central Bank of Ireland November 22, 2012 ICON fined €10,000 by Central Bank for breaches of market abuse rules RTE May 8, 2012 Address by Peter Oakes, Director of Enforcement, to the Association of Compliance Officers (‘The role of enforcement and activities of the Enforcement Directorate’) (Thought Leadership) Central Bank of Ireland November 19, 2012 Ulster Bank fined €1.96m for breaches of financial regulations RTE October 4, 2012 Central Bank fines Bank of Ireland Mortgage Bank for breaches RTE June 21, 2012 UBS fined for anti-money laundering breaches RTE April 2, 2012 Central Bank fines life company (Alico) more than €3 million. The Central Bank has fined a life company €3.2 million for breaches of financial regulation. Business Post March 18, 2012 CHC investors could face long delay on payout Business Post January 22, 2012 The financial heads that didn't roll Business Post December 19, 2011 Insurance firm may have to refund €2m RTE December 11, 2011 Another broker in line for censure Business Post July 22, 2011 Central Bank fines Aviva Investors Ireland RTE June 9, 2011 Central Bank to give pre-crisis directors initial written warning Independent April 9, 2011 Financial Regulator to begin flexing its new muscles Business Post June 28, 2010 Key appointments made at Central Bank RTE April 17, 2010 Banks seek loopholes to escape tracker mortgages Business Post March 02, 2009 New banking oversight commission planned RTE December 5, 2009 The Inquisitor: Honohan’s home truths rattle the bankers’ cages Business Post June 30, 2007 FitzPatrick rails against ‘corporate McCarthyism’ Business Post September 23, 2006 Customers take hits from scams Business Post July 30, 2005 Are 100% mortgages a fraud risk? Business Post

0 Comments

Back to Blog

Legend Trading Europe, a Dublin-based fintech that helps businesses move money between traditional payment systems and digital assets, has secured €3.3 million to expand its Irish operations. The firm, a subsidiary of US-regulated cryptocurrency trading platform Legend Trading, is to use the financing in part to pursue an e-money licence from the Central Bank of Ireland in a move that will allow it to offer both fiat and stablecoin payment services from a single regulated entity. Legend has been supervised by the Central Bank of Ireland since 2024 and licensed by the regulator under the EU's MiCA crypto rules since late last year.

Speaking to the Business Post, Ciaran O'Hare, the firm's chief executive, said the e-money licence application builds on that existing regulatory foundation and "reinforces Ireland's role as the company's European headquarters."

"We employ 12 people here at the moment working across risk, compliance, AML (anti-money laundering) and finance, and a very strong board that includes Peter Oakes and Valerie Lyons," said O'Hare. He said the company intends to expand its compliance, risk and engineering teams in Dublin. "I expect that we will double headcount or possibly even triple it over the next two years as we're looking at how we might move some functions that currently sit in the US over here so that we are fully resourced in every department," O'Hare said. Legend's parent is a global crypto infrastructure firm providing fiat–crypto and crypto–fiat rails to retail, institutional clients, high-net worth individuals, exchanges, wallets, and fintechs. Legend has facilitated tens of billions of dollars in transactions since it was founded six years ago and is used by more than 1,000 institutional traders. O'Hare said combining electronic money and digital asset services under a single regulated entity would simplify how businesses move between fiat and digital assets. "We're seeing growing demand from businesses that want access to both traditional payment infrastructure and stablecoin settlement within a regulated framework. Our focus is building that infrastructure within a regulated Irish entity under the supervision of the Central Bank of Ireland," he said. Hao Chen, founder of Legend Trading, said that having spent the last seven years building liquidity and trading infrastructure for digital assets, the next stage is "enabling businesses to access payments, treasury and settlement services that bridge traditional financial systems and digital asset networks." "Europe is becoming one of the most important markets for that evolution," he said. Source: Business Post, Charlie Taylor "Legend Trading secures €3m to boost Dublin operations" 13 June 2026

Back to Blog

The Central Bank of Ireland is growing anxious about the risks to Irish crypto firms of the war in Iran. The regulator on Thursday wrote to chief executives of authorised Irish crypto asset service providers warning that the US-Israel strikes on Iran may have a “detrimental impact on crypto markets and firms’ ability to operate effectively”. The CBI questioned crypto firms about the impact the conflict – and the market turbulence that has followed – has had on their businesses. It also asked the chief executives if they have “assessed and stressed the potential impact of a prolonged war on the firm’s business model, profitability, and operations”, and whether they have conducted a cyber-risk assessment. “What actions are the firm taking to ensure the ongoing resilience of the firm’s business model, profitability and operations from global and geopolitical events?” the CBI asked. It gave crypto firms 24 hours to respond to its questions. The strikes on Iran by Israel and the US have worried investors over recent weeks, with stocks seesawing as oil prices have spiked. Bitcoin, the most valuable cryptocurrency by market cap, has outperformed gold and stocks since the beginning of the war. Bitcoin has risen about 7 per cent since the war started on February 28, trading at close to $72,000 on Friday afternoon. US investigators are looking at whether crypto platforms have enabled state-linked players to evade sanctions when seeking to move money abroad, access hard currency or procure goods, Reuters reported last month. TRM Labs, the American blockchain intelligence platform, has estimated that there was around $10 billion of crypto activity in Iran last year, against $11.4 billion in 2024.

Joe McCann, managing director of Irish cybersecurity firm Intercept Technologies, said the conflict presented “heightened risks” to crypto firms, including those in Ireland. McCann said he attended a recent supervisory briefing held by the CBI, adding: “They’re now talking more than they ever had about cyber resilience. “Ultimately, the risk posed to crypto asset service providers, even from a financial services aspect, is significantly higher than any others,” he said. “They’re constantly being targeted.” McCann said that for crypto firms, guarding against cyber attacks is no longer sufficient. “Protecting isn’t the only thing anymore,” he said. “It’s actually about monitoring and reporting.” Peter Oakes, the founder of Fintech Ireland, said it was “no great shock” that regulated crypto firms had received letters. “All of them have just passed through authorisation and should be treated like for like as other regulated fintech firms,” he said. “The letter is equally relevant to the trading desks of investment firms and some payments firms.” A spokesman for the CBI declined to comment on the specifics of its letter to crypto firms, but said the regulator is continuing to “monitor developments relevant to financial firms and services”. “The speed of current geopolitical developments calls for a clear understanding by firms and supervisors of the channels through which multi-faceted geopolitical risks can transmit to their organisations, and the consequent adaptability and resilience they need to nurture so they can respond to, and withstand, unexpected events,” he said. “This is a routine supervisory focus at a time of fast-moving global developments.” Source: Business Post. Donal MacNamee, 13 March 2026 "Central Bank warns Irish crypto bosses over Iran war risk (Business Post)"

Back to Blog

“With crypto firms able to passport their services across the EEA, there is the possibility of thousands of fintechs doing business here while being authorised elsewhere,” Non-executive director Peter Oakes, founder of Fintech Ireland and former enforcement director at the Central Bank of Ireland comments within an insightful piece by Charlie Taylor of the Business Post. In terms of optics, Coinbase’s decision to relocate doesn’t look great for Ireland Inc. But in truth, it ultimately might not matter. Peter Oakes, a former Central Bank enforcement director and founder of Fintech Ireland, an industry group, said that while many exchanges may get authorised elsewhere, there is still the potential for Ireland to become a hub for compliance and risk management. “With crypto firms able to passport their services across the EEA, there is the possibility of thousands of fintechs doing business here while being authorised elsewhere,” he said, noting that Coinbase was still keeping a big presence locally. Even so, this is a debate that is unlikely to end any time soon. Source: https://www.businesspost.ie/tech/charlie-taylor-is-the-central-bank-pushing-fintechs-away-from-ireland/ "Is certain negative narrative from 'unnamed insiders' about the Central Bank of Ireland informed, wise and indeed accurate?" Is certain negative narrative from 'unnamed insiders' about the Central Bank of Ireland informed, wise and indeed accurate?

Back to Blog

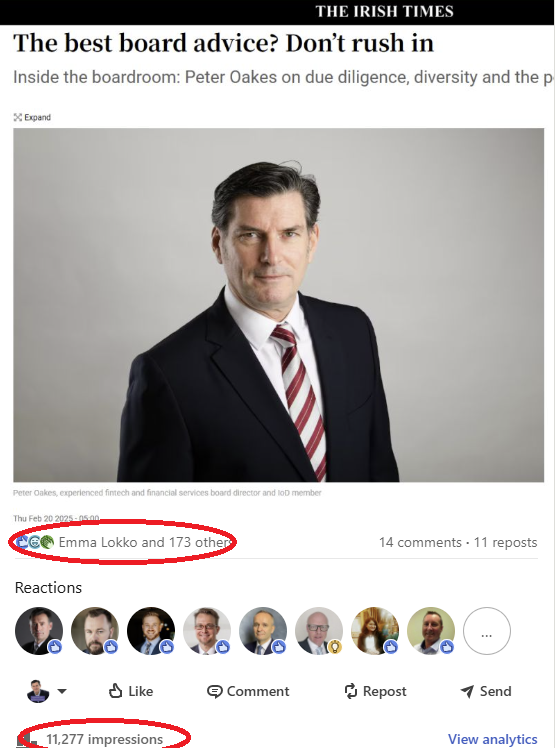

Inside the boardroom: Peter Oakes on due diligence, diversity and the power of a continuous learning (published 20 February 2025) Many thanks Caroline Kinsella of the Institute of Directors Ireland for the opportunity to provide some personal insights on the role of an Independent Non-Executive Director in the Irish Times. And thanks to Caroline Spillane for her kind words in her post yesterday when Caroline circulated the article. Experienced fintech and financial services board director Peter Oakes advises non-executive directors (NEDs) to be selective when considering board appointments. “Quite an amount of due diligence needs to be done on the company first,” he says. “If you think you are just joining a club, you’re better off not doing it. If you take on risks you don’t understand you can end up in the papers for all the wrong reasons. You must make sure it’s the right fit for you and that you have something to offer the company or the market it operates in, something they don’t already have on the board. You should add to the diversity of experience and thought on the board.” A long-time member of the Institute of Directors (IoD) Ireland and founder of industry representative body Fintech Ireland, Oakes is currently a non-executive director of several regulated fintech and financial services firms while also providing expert advice regulatory compliance to clients in those industries. “IoD membership has been invaluable throughout my career,” Oakes shares. “It provides access to crucial resources, networks, and educational programmes that keep me at the top of my game, especially when it comes to governance and regulatory knowledge. Before accepting any board position, I always ensure that I am equipped with the right skills and insights to add meaningful value.” He recalls one of the first offers he received to join a board. “I was about to join it, but I couldn’t get my head around some important aspects of its business model and what the duties and function of an independent non-executive director (INED) on its board would be, so I turned down the opportunity. A couple of years later, the company ended up in trouble with the regulator. The best advice is not to rush into it. If you find you have accepted every directorship offered, that should be a warning bell.” And I highly recommend joining the Institute of Directors in Ireland if you are serious about joining a board. Continue reading at the sources below. Sources:

Irish Times - https://www.irishtimes.com/advertising-feature/2025/02/19/the-best-board-advice-dont-rush-in/ Institute of Directors Members' Profiles - https://www.iodireland.ie/membership/member-profiles/peter-oakes-member-profile

Back to Blog

It is not often that one hears of fintechs having sympathy for the very people they set out to disrupt: bankers. However, a case in Ireland against senior banker David Guinane has set alarm bells ringing at fintechs, insurers, asset managers and funds companies. Non-executive director Peter Oakes is a former enforcement director at the Central Bank of Ireland. Source: Last week, it was revealed that the former CEO of Permanent TSB “participated” in a breach of regulation admitted by his former employer in 2019.

Three years after PTSB held up its hands to 42 regulatory breaches between 2004 and 2018, and agreed to pay €21mn in fines, the Irish regulator went after Guinane personally. The Central Bank of Ireland opened an inquiry to determine Guinane’s role in the affair, which impacted 2,007 tracker mortgage customers and led to €54mn in redress and compensation. The inquiry’s chair, esteemed barrister Peter Hinchcliffe, found that on the balance of probabilities, Guinane did not ensure his bank acted fairly in the best interest of its customers under a general principle of Irish consumer protection law. The finding sets a precedent for anyone working in regulated financial services in Ireland and marks a step-up in enforcement from the supervisor “Okay with that” The facts turn on an ambiguously worded special condition known as the “SC706 clause” in certain mortgage holders’ contracts and a three-word email response. The regulator’s case against the banking chief rests largely on what has been coined the ‘smoking gun’: “Okay with that.” Guinane emailed these three words 16 years ago when asked to sign off on a proposal from his management team. His legal staff had reviewed the proposal to deal with certain mortgage customers who wanted to return to their original low tracker-rate loan after coming off a period of fixed rates. The bank’s default position was to place them on a higher standard variable rate. What should concern fintech executives and others at regulated financial services providers operating in Ireland is how the outcome of this case applies to their industries — specifically personal accountability. Since the Irish regulator’s new Senior Executive Accountability Regime, analogous to the UK’s Senior Managers Regime, came into force in 2024, certain senior managers and board members can face proceedings independent of their employer. Most regulated fintechs currently fall outside SEAR, which is meant primarily for banks, insurers and investment managers, but the Guinane case sets an alarming new precedent. Despite Guinane’s conduct predating SEAR by more than a decade, he has been found personally liable for PTSB’s regulatory breaches and faces a fine of up to €500,000. For those in management at regulated fintechs, the case is a reminder that they can be pursued and held accountable for failures by their company, even though fintechs fall outside the new SEAR regime. What’s more, the maximum fine went up to €1mn in July. How was Guinane deemed accountable? Hinchcliffe had to consider whether the banker was “a person concerned in the management” of PTSB. While Guinane held the position of CEO, the ultimate responsibility for regulatory compliance at PTSB fell to its owner, Irish Life & Permanent Group. While Guinane did not sit on the board of IL&PG, the inquiry ruled he fell within its jurisdiction. These failures derive from breaches of prescribed contraventions of “relevant obligations” — for which there is no comprehensive list readily available. Recent comments from the CBI’s former deputy governor, Sharon Donnery, now a senior executive at the European Central Bank, give some clues about the regulator’s thinking. Donnery told the Fintech Ireland Summit in November that, in an age of rapid technological advancement, the “basics” — good governance, risk management and consumer protection — “remain true”. Fintechs drew a sharp breath of air when she singled them out: “Unfortunately, it does have to be said that our supervisory experience continues to point to instances of [fintech] firms failing to provide the basic statutory obligations around protecting people’s money.” Donnery’s pointed comments and now the Guinane precedent mean that fintech executives — not just the “big boys” of banking, insurance and investment services — are on notice that they too can be proceeded against for breaching Ireland’s consumer protection code. Firm up internal processes Many have expressed sympathy for Guinane, whom the inquiry confirmed neither acted dishonestly nor had any intention to harm or take advantage of customers. Of particular worry for senior executives is a comment by Hinchcliffe that Guinane was entitled to receive better support from within IL&PG. Now a sanction hearing will determine what penalty, if any, should be imposed. It could range from a caution or reprimand to a maximum cash fine of €500,000 through to being disqualified from working in management at a regulated service provider. The kicker is a potential costs order. A recent shake-up at the CBI offers little hope of leniency for Guinane. The enforcement directorate has a new leader in the form of Colm Kincaid from the consumer protection directorate. He replaces a fellow lawyer, Seána Cunningham, who now leads the insurance supervision directorate. However, nothing here suggests any change to the enforcement unit’s appetite and operations for pursuing individuals. Finally, fintech executives must actively consider their internal procedures. They need to demonstrate regulatory compliance and, more importantly, prove they have considered the implications for customers when signing off on business strategies. One wonders whether this will be enough given comments by Mr Guinane legal team that he has been singled out and that an appeal is inevitable. After all, no other banker in Ireland has faced inquiry, despite more than half a dozen banks being hit with €280mn of fines over the exact same scandal.

Back to Blog

Peter Oakes, former director of AML enforcement at the Central Bank of Ireland, told moneylaundering.com that regulators expect compliance personnel to fully apprise themselves of the purpose, capabilities and limitations of any regtech their institutions acquire, and do not wait around for an internal audit to identify any problems. “Unthinking” reliance on new technologies landed roughly half of the more than 250 financial services companies found to have breached anti-money laundering rules in the EU this year in hot water with their national supervisors, a senior regulator has warned.

Carolin Gardner, head of AML at the European Banking Authority in Paris, told ACAMS moneylaundering.com that concerns now abound that financial institutions frequently fail to deploy the latest transaction-monitoring software and other innovative tools effectively, creating gaps in their compliance programs that can persist “for a significant period of time.” “One of the challenges, based on what supervisors are telling us, is that technology is being employed before it’s properly tested, and that [it] then has the potential to actually weaken institutions’ systems and controls,” said Gardner. In January 2022, as part of a broader effort to strengthen and harmonize AML oversight across the European Union, the European Banking Authority, or EBA, launched EuReCA, a bloc-wide database where national regulators log any “material weakness es” found at financial institutions, and the remedial measures or other steps they took in response to them. Regulators in the bloc’s 27 nations have uploaded a combined 771 AML violations at 256 banks, money services businesses and other financial institutions on the database so far this year. At around half of those companies, improper use of new regulatory-compliance technology, also known as regtech, laid at the heart of the breaches. Artificial intelligence-driven software, advanced data-analytics tools and other regtech products hold the promise of radically improving customer-identification and -verification processes, bolstering detection of potentially illicit transactions and helping compliance officers untangle complex corporate structures. But national supervisors have observed a substantial uptick of cases in which banks and fintechs neglected to check whether their newly acquired, compliance-related technologies delivered as promised, and failed to ensure that senior managers consistently monitored their use. “We are in favor of technology, we don’t think the fight against financial crime has a future without it and we have seen excellent examples where it works fantastically,” said Gardner. “Our concern at the moment is that not everyone is using technology in the right way.” EU supervisors have reported 377 enforcement actions or other supervisory responses to EuReCA since January. Details of many of the associated violations show that regtech-related shortcomings appeared in all areas of AML compliance. “It’s difficult to pinpoint exactly what’s going wrong where, because it’s really a little bit of everything,” said Gardner. “This is clearly an area where we feel we need to intervene, and we need to intervene fast.” Regtech-related problems have also become a regular topic of discussion at the EU’s supervisory “colleges,” forums where national regulators share information (https://www.moneylaundering.com/news/eu-aml-supervisory-colleges-grow-in number-effectiveness-eba/) on the AML programs of financial institutions that operate across borders. Peter Oakes, former director of AML enforcement at the Central Bank of Ireland, told moneylaundering.com that regulators expect compliance personnel to fully apprise themselves of the purpose, capabilities and limitations of any regtech their institutions acquire, and do not wait around for an internal audit to identify any problems. “They normally already have a framework for product governance elsewhere, but firms need to extend that to any regtech offerings they bring on board,” said Oakes, now a consultant in Dublin. “They also need to identify it [new regtech] as a risk, so that there’s a discussion around monitoring and regular testing.” The EBA plans to conduct additional research on the problematic trend ahead of publishing an “opinion” on emerging money laundering- and terrorist financing-related risks next year. Contact Koos Couvée at [email protected]

Back to Blog

Sharon Donnery: deputy governor, Central Bank of Ireland said: ‘Contrary to some beliefs, central banks and regulators welcome innovation.’ According to Fintech Ireland, a body set up to promote innovation, which is led by former central banker Peter Oakes and co-organised the conference, there are 80 authorised fintechs in Ireland. Many Irish fintechs are still failing to fulfil their “basic statutory obligations” when it comes to protecting consumers’ money, the deputy governor of the Central Bank of Ireland (CBI) has warned. Sharon Donnery, the person in charge of financial regulation at the CBI, issued a sharp rebuke to some rms in the sector at the Fintech Ireland Summit in Dublin on Thursday. Some rms, she said, have still not understood the regulatory principles of good governance, risk management and consumer protection, with others failing to “sufficiently” deliver them. Donnery did, however, welcome interest from fintechs in the CBI’s so-called innovation sandbox – a hub where rms can test out new products under regulatory supervision – and disclosed that nearly 40 rms had applied. “Contrary to some beliefs, central banks and regulators welcome innovation,” Donnery said at the conference. “While we don’t embrace it indiscriminately, our mandate is to deliver in the public interest.” Fintechs have sometimes questioned the CBI’s “defensive” approach to firms seeking authorisation.

According to Fintech Ireland, a body set up to promote innovation, which is led by former central banker Peter Oakes and co-organised the conference, there are [80] authorised fintechs in Ireland. Miriam Dunne, the regulator’s head of innovation and stakeholder engagement, admitted last year the sector’s development posed a “challenge for our mindset” and noted that the regulator is “committed more now to fostering innovation”. Donnery, though, struck a more hawkish tone towards fintech regulation on Thursday, noting the CBI’s expectations for the sector “are not new”. “Unfortunately it does have to be said that our supervisory experience continues to point to instances of rms failing to provide the basic statutory obligations around protecting people’s money,” she said. In an age of rapid technological advancement, Donnery also said the “basics” – good governance, risk management and consumer protection – “remain true”. “While these principles are general, our supervisory experience tells us they’re not always understood. “Or, if understood, they’re not necessarily sufficiently delivered,” she said. Donnery said that while it was understandable some ntechs would focus on fast expansion, “growing the business without also properly growing its control frameworks is not really a recipe for sustainable success”. “And indeed it is not acceptable for regulated providers of nancial services,” she added. Donnery said both the CBI and regulated rms are responsible for looking after people’s money and nancial wellbeing. “For those that are trusted with that responsibility, there are some basic expectations – in particular that you’re well-run, have good governance and risk management capabilities commensurate with,” she said. Despite that, Donnery said the CBI was “delighted” at the breadth of companies that applied for its innovation sandbox, for which applications closed in recent weeks. “Almost 40 [ rms] in total” applied for the programme, she said, including companies from Ireland, the EU and the UK. Applicants represented a “really wide variety of rms – from start-ups to established fintechs, to incumbent financial services providers,” she said, adding that the regulator would announce the selected participants in the coming weeks.

Back to Blog

Charlie Taylor, Technology Editor of the Business Post writes: Ireland’s tech scene is one that has burgeoned in recent years and one in which we can be justifiably proud. It spans multiple disciplines and covers businesses both big and small. For the first time at Connected, we’ve assembled a list of who we think are the most impactful people in Ireland’s tech scene currently. As with all lists, this isn’t the final word on the issue but rather a starting-off point for a deeper conversation about what it is that makes Ireland’s tech sector so strong. In compiling this ranking, we’ve consulted widely and relied on a range of criteria. Many of those here could arguably fit under multiple categories. In addition, on another day you could arguably find as many more people again who would justify a spot on this list that aren’t present. These factors in themself show the strength of the tech scene in Ireland. However, a line has to be drawn somewhere and we’re the ones drawing it. Read more here

Back to Blog

Interesting to see that while the cost for fake/stolen passports and drivers licences have increased (almost double), the cost to hack someone’s email account dropped 60% in 2023. At least there is no escaping the laws of economics for bad actors! See this YouTube link for more - https://www.youtube.com/watch?v=MWb7dUUXO2M "Inflation is hitting everyone hard it seems — even scammers. New data reveals the cost of fake or stolen documents like passports and driver's licenses on the dark web has gone up significantly, as demand increases and the number of people being scammed decreases. According to a report from accounting firm BDO, the average cost of buying a fake or stolen passport on the dark web is now $2,372 (up from $1,399 in the previous quarter), while a driver's license will set you back $844 (up from $465). But it's a competitive market and in some cases prices have dropped. The average cost to hack into someone's email is now just $262 (down from $668), according to BDO.".  BDO's Stan Gallo said the dark web is “like any other market environment where there's supply and demand". "He believes increased awareness of scams over the past year, high profile crackdowns and more embedded security measures in some ID documents has made it harder for criminals to get away with obtaining, selling and using fraudulent documents and has therefore pushed the price up.

"It's like any other market environment where there's supply and demand," he told the ABC. "And if there's a restricted supply and the demand is still there, then the price goes up. If things are easier to get, then the price will come down because it will drive competition." He notes anyone who tries to buy fake passports or conduct other illegal activities on the dark web must accept a significant risk and face repercussions including possible imprisonment.". Read more here https://www.abc.net.au/news/2024-03-25/criminal-inflation-stolen-data-price-increase-dark-web-scams/103620916 |

© Peter Oakes (all rights reserved)

There is no consent nor legitimate interest right available to data vendors (e.g Zoominfo.com) and others to use email addresses, phone numbers and address details to send unsolicited marketing communications. This notice prevents you from claiming a business-to-business avenue to send unsolicited communications to any contact details appearing on this website. The email address PETER AT PETEROAKES.COM is a personal email address and is also protected by GDPR rights.

Privacy Statement.

There is no consent nor legitimate interest right available to data vendors (e.g Zoominfo.com) and others to use email addresses, phone numbers and address details to send unsolicited marketing communications. This notice prevents you from claiming a business-to-business avenue to send unsolicited communications to any contact details appearing on this website. The email address PETER AT PETEROAKES.COM is a personal email address and is also protected by GDPR rights.

Privacy Statement.