|

Back to Blog

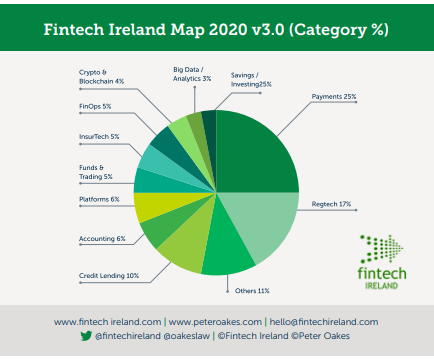

Why would one start an article about fintech referencing Covid-19? The fact is that the virus is acting as both a headwind and tailwind for fintech companies operating from Ireland and internationally. The impact of the virus over the last month and a half on fintech has shone a spotlight on many aspects of the ecosystem that might not have otherwise come to our attention. In the current climate Ireland must also be mindful of any potential slippage of its position as a global fintech player garnered from recent years of excellent work. Let’s start with an overview of fintech. The word fintech came to prominence after the last financial crisis, particularly noticeable from 2012 onwards. Yet there were many examples of ‘financial technology’, shortened to “fintech”, existing well before the start of the last financial crisis. A number of these fintech businesses date back to the latter part of the 1980’s. Examples include the internet and phone retail bank First Direct (a division of HSBC) which kicked off in 1989 and today regularly achieves high satisfaction rates in financial surveys. Ireland too served as HQ to a pioneer challenger bank, First-e, which despite great promise was a casualty of the dot.com boom.  What does the Irish fintech scene look like? The consensus is that Ireland is home to somewhere between 220- 250 indigenous fintech companies and that together with international fintech companies in Ireland, the number is probably around 400. It is difficult to give an exact figure if only because the word “fintech” is a broad-church. The word captures, (a) the new nonbank disruptors which focus on discrete parts of the banking value chain, e.g. payments, wealth management, treasury services and credit and lending; (b) the new breed of digital only (non-branch) challenger banks entering both retail and business banking; and (c) the incumbent banks (sometimes referred to as legacy banks) embarking - with various degrees of success – on digital transformation journeys. The recent release in April of the 2020 edition of the Fintech Ireland Map4 identified 230 indigenous / Irish controlled fintech companies. This was an increase of 30% from the previous year. The Map is supported by both research and a survey. The criteria to meet to join the Map is challenging. Entrants must be fintech companies with a proprietary product or service. Broadly speaking the fintech companies operate across 12 categories, being Credit & Lending; Platforms; Funds & Trading; Crypto & Blockchain; FinOps (Financial Operations); InsurTech (Insurance Technology); Accounting; Payments; RegTech (Regulatory Technology); Savings / Investing; Big Data / Analytics; and Others. The number of firms in each category is shown in the diagram below. IF YOU LIKE WHAT YOU HAVE READ SO FAR, CONTINUE READING AT THE SOURCE (FREE - NO ADS) AT COMPLIREG

0 Comments

Back to Blog

UK fintech and financial services, it's time to advance plans to establish a presence in Ireland!

See:

The Irish Government is to restart preparations for a no-deal Brexit, Ministers will be told today, as negotiations between the UK and EU on a trade deal show little signs of progress. Ireland's second most senior Minister will brief the Irish Cabinet on the state of the negotiations in Brussels, and tell Ministers that preparations at ports and airports will need to be stepped up as Ireland emerges from the coronavirus lockdown. Mr Coveney will outline two potential scenarios that could unfold in the second half of the year: either the two sides reach a “basic” free trade agreement that includes zero tariffs and zero quotas on goods, including fish, or they fail to reach agreement, in which case a no-deal Brexit will come into operation at the beginning of 2021. If there is a no-deal Brexit, Ministers will be told, Irish agrifood exports to the UK could be hit with some €1 billion in tariffs. UK Extension? The UK must decide by the end of June if it wishes to seek an extension to the present transition phase, during which, although legally outside the EU, the UK applies the laws and receives the benefits of the EU single market. However, the UK government has said it will not under any circumstances apply for an extension, meaning there are just seven months left to reach a comprehensive free trade agreement. Such a process normally takes several years. There has been little progress so far in the negotiations, which began in March, and Mr Coveney is likely to offer a gloomy prognosis to Ministers when they meet today. Of the four negotiating rounds scheduled to take place before the end of June, three have been completed, but they have achieved little agreement on anything of substance. The next round starts next week. https://www.irishtimes.com/news/politics/irish-planning-for-no-deal-brexit-to-restart-as-eu-uk-talks-go-badly-1.4265185 |

© Peter Oakes (all rights reserved)

There is no consent nor legitimate interest right available to data vendors (e.g Zoominfo.com) and others to use email addresses, phone numbers and address details to send unsolicited marketing communications. This notice prevents you from claiming a business-to-business avenue to send unsolicited communications to any contact details appearing on this website. The email address PETER AT PETEROAKES.COM is a personal email address and is also protected by GDPR rights.

Privacy Statement.

There is no consent nor legitimate interest right available to data vendors (e.g Zoominfo.com) and others to use email addresses, phone numbers and address details to send unsolicited marketing communications. This notice prevents you from claiming a business-to-business avenue to send unsolicited communications to any contact details appearing on this website. The email address PETER AT PETEROAKES.COM is a personal email address and is also protected by GDPR rights.

Privacy Statement.