|

Back to Blog

Who wants to buy a bank? Web browser Opera does as it continues inroads into banking and fintech9/7/2020  Who wants to buy a bank?It seems that web browser Opera does after announcing investment in and agreement to acquire Fjord Bank, a Norwegian capital bank established in Lithuania regulated by the Lietuvos bankas / Bank of Lithuania and the European Central Bank. Fjord Bank was founded in March 2017 and only established in Lithuania in 2019. Opera, headquartered in Oslo, Norway, announced its intention to purchase Fjord Bank subject to regulatory approval. Opera says that "The acquisition will enable Opera to further accelerate its fintech operations in Europe by launching new, disruptive services aimed at improving consumers’ personal finances." Innovative fintech in Europe and beyond could also be acquired as Opera. Opera first ventured into the fintech space in Europe acquiring Estonian fintech Pocosys which provides digital wallets, payment technology and banking-as-a-service software. At the time of the Pocosys acquisition Opera's Krystian Kolondra said "The way we use financial services is starting to change rapidly ...We see a lot of potential for better and easier services. Needless to say we are excited about our future fintech plans associated with Pocosys and our existing brand.” The Pocosys deal also included an agreement to take over its startup’s sister company which holds a payment institution license and provides financial services in the European Union. "Opera has been making innovative browsers and apps for 25 years. Our browsers are the personal choice of millions of people who prefer them over those that come preinstalled on their devices,” said Krystian Kolondra, EVP Opera. “Looking at the fintech space in Europe, we believe it needs more and bigger challengers who should provide people with smarter and empowering solutions for their personal finances." Why is Opera entering the challenger bank and fintech space?pera says that it has growing user base of more than 50 million monthly active browser users in Europe. Its move into challenger banking and fintech is owed to its current and ambition to grow its position as a top European top consumer technology. Opera is ranked 6th in terms of usage share of desktop browsers and 5th in terms of usage share of mobile browsers according to Wikipedia. Together with the acquisition of the Estonian fintech company PocoSys, the acquisition of AB Fjord Bank means Opera will become a fuller suite financial services provider. We will see soon see Opera via the acquisition of the specialized bank launching its first deposit and loan service in Lithuania this summer 2020. “We are looking forward to joining the Opera family, and accelerating its plans to grow its unique product offering”, said Veiko Kandla, CEO of AB Fjord Bank, “With the support of Opera, we are also excited to launch our first banking services in Lithuania this summer”. Further detail on the Opera and AB Fjord Bank investment and share purchase agreementOpera and AB Fjord Bank entered into an investment and share purchase agreement on May 29th 2020. Opera acquired a 9.9% interest in AB Fjord Bank via a share subscription which was completed on 3 July 2020. Completion of the acquisition of the remaining 90.1% of Fjord Bank is pending regulatory approval. An result of Opera' recent fintech activity, it has created demonstrable fintech bridge links between Norway, Estonia, Lithuania and Sweden as well as creating three European fintech hubs for fintech services in: Tallinn, Estonia; Vilnius, Lithuania; and Gothenburg, Sweden. Further reading & sources:  This blog written by Peter Oakes of CompliReg, Fintech Ireland and Fintech UK Peter advises on Lithuanian EMI/PI issues and advised on the authorisation of one Lithuania's first special bank authorisations. If you require a licence to operate in Lithuania, Ireland, Cyprus, Malta or the UK, see our Authorisation Page. We have a great network of experts in each country too, from lawyers, to accountants to technical experts. And get in contact if you have a question about this blog.

0 Comments

Back to Blog

Peter Oakes, Enforcement Expert & Lawyer Peter Oakes, Enforcement Expert & Lawyer Here's an enforcement action which will serve as a useful typology for fitness and probity, not to mention culture and behavior, as Ireland heads towards a Senior Executive Accountability Regime by Peter Oakes Peter is was appointed the first Director of Enforcement and Ant-Money Laundering at the newly reconstituted Central Bank of Ireland in 2010, where he led and developed the creation and staffing of the new Enforcement and Anti-Money Laundering Directorate with responsibility for delivering administrative sanction procedure enforcement actions, unauthorised providers actions, fitness and probity supervisory and enforcement actions and development of new regulatory laws. Peter has worked on a number of regulatory enforcement matters since leaving the Central Bank and is available to advise and represent on such matters. Read more here Bullet Point Summary

Continue reading this blog at CompliReg

Back to Blog

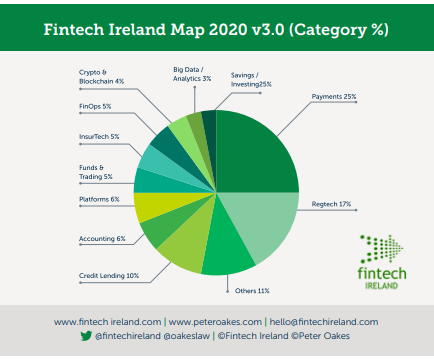

Why would one start an article about fintech referencing Covid-19? The fact is that the virus is acting as both a headwind and tailwind for fintech companies operating from Ireland and internationally. The impact of the virus over the last month and a half on fintech has shone a spotlight on many aspects of the ecosystem that might not have otherwise come to our attention. In the current climate Ireland must also be mindful of any potential slippage of its position as a global fintech player garnered from recent years of excellent work. Let’s start with an overview of fintech. The word fintech came to prominence after the last financial crisis, particularly noticeable from 2012 onwards. Yet there were many examples of ‘financial technology’, shortened to “fintech”, existing well before the start of the last financial crisis. A number of these fintech businesses date back to the latter part of the 1980’s. Examples include the internet and phone retail bank First Direct (a division of HSBC) which kicked off in 1989 and today regularly achieves high satisfaction rates in financial surveys. Ireland too served as HQ to a pioneer challenger bank, First-e, which despite great promise was a casualty of the dot.com boom.  What does the Irish fintech scene look like? The consensus is that Ireland is home to somewhere between 220- 250 indigenous fintech companies and that together with international fintech companies in Ireland, the number is probably around 400. It is difficult to give an exact figure if only because the word “fintech” is a broad-church. The word captures, (a) the new nonbank disruptors which focus on discrete parts of the banking value chain, e.g. payments, wealth management, treasury services and credit and lending; (b) the new breed of digital only (non-branch) challenger banks entering both retail and business banking; and (c) the incumbent banks (sometimes referred to as legacy banks) embarking - with various degrees of success – on digital transformation journeys. The recent release in April of the 2020 edition of the Fintech Ireland Map4 identified 230 indigenous / Irish controlled fintech companies. This was an increase of 30% from the previous year. The Map is supported by both research and a survey. The criteria to meet to join the Map is challenging. Entrants must be fintech companies with a proprietary product or service. Broadly speaking the fintech companies operate across 12 categories, being Credit & Lending; Platforms; Funds & Trading; Crypto & Blockchain; FinOps (Financial Operations); InsurTech (Insurance Technology); Accounting; Payments; RegTech (Regulatory Technology); Savings / Investing; Big Data / Analytics; and Others. The number of firms in each category is shown in the diagram below. IF YOU LIKE WHAT YOU HAVE READ SO FAR, CONTINUE READING AT THE SOURCE (FREE - NO ADS) AT COMPLIREG

Back to Blog

WATCH VIDEO HERE

Recorded for ACAMS 24+ Financial Crime Marathon (2 & 3 June 2020). This video is a discussion between Shilpa Arora, AML Director - Europe, Middle-East and Africa at ACAMS and Peter Oakes (Fintech Ireland, Fintech UK & CompliReg) on The Latest and Greatest in the World of Fintech. Sound starts at 25 seconds into video following title slides. Big thanks to ACAMS for the invitation to join such an excellent event. WATCH VIDEO HERE

Back to Blog

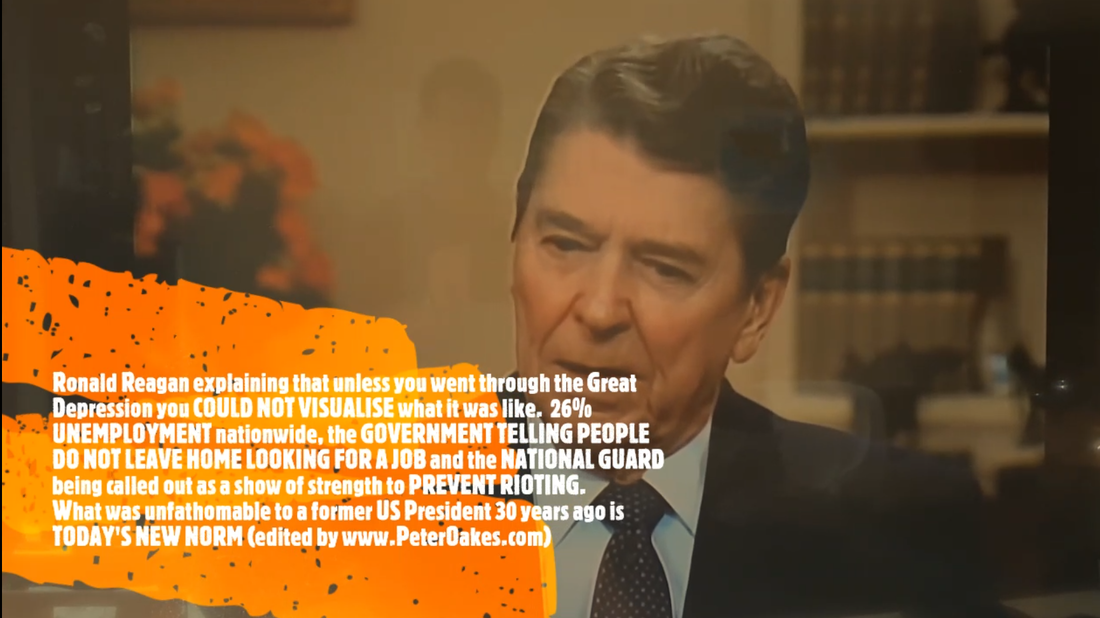

Former US President Ronald Reagan eerie interview - parallels with Covid19 & George Floyd riots30/5/2020  At some point my post today on Linkedin will disappear of an interview of former US President (1981-1989) by Tom Brokaw from the Reagan Library which I located on Youtube. Ronald Reagan explaining that unless you went through the Great Depression you COULD NOT VISUALISE what it was like. 26% UNEMPLOYMENT nationwide, the GOVERNMENT TELLING PEOPLE DO NOT LEAVE HOME LOOKING FOR A JOB and the NATIONAL GUARD being called out as a show of strength to PREVENT RIOTING. What was unfathomable to a former US President 30 years ago is TODAY'S NEW NORM (edited by www.PeterOakes.com / Peter Oakes)

Back to Blog

UK fintech and financial services, it's time to advance plans to establish a presence in Ireland!

See:

The Irish Government is to restart preparations for a no-deal Brexit, Ministers will be told today, as negotiations between the UK and EU on a trade deal show little signs of progress. Ireland's second most senior Minister will brief the Irish Cabinet on the state of the negotiations in Brussels, and tell Ministers that preparations at ports and airports will need to be stepped up as Ireland emerges from the coronavirus lockdown. Mr Coveney will outline two potential scenarios that could unfold in the second half of the year: either the two sides reach a “basic” free trade agreement that includes zero tariffs and zero quotas on goods, including fish, or they fail to reach agreement, in which case a no-deal Brexit will come into operation at the beginning of 2021. If there is a no-deal Brexit, Ministers will be told, Irish agrifood exports to the UK could be hit with some €1 billion in tariffs. UK Extension? The UK must decide by the end of June if it wishes to seek an extension to the present transition phase, during which, although legally outside the EU, the UK applies the laws and receives the benefits of the EU single market. However, the UK government has said it will not under any circumstances apply for an extension, meaning there are just seven months left to reach a comprehensive free trade agreement. Such a process normally takes several years. There has been little progress so far in the negotiations, which began in March, and Mr Coveney is likely to offer a gloomy prognosis to Ministers when they meet today. Of the four negotiating rounds scheduled to take place before the end of June, three have been completed, but they have achieved little agreement on anything of substance. The next round starts next week. https://www.irishtimes.com/news/politics/irish-planning-for-no-deal-brexit-to-restart-as-eu-uk-talks-go-badly-1.4265185

Back to Blog

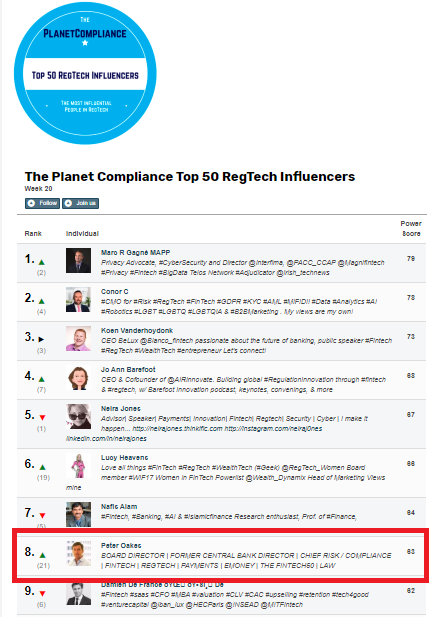

Thanks CompliReg for the shout out - https://complireg.com/blogs--insights/peter-oakes-in-top-10-regtech-influencers-planet-compliance

Back to Blog

Australian Bank giant Westpac is expecting to fork out more than $1 billion as a result of its money laundering scandal and admitting to 23 million anti-money laundering breaches.

It's not just story about culture, conduct risk and financial crime risks. Far more importantly, it is a story of shame, leadership failure and financial pain for Westpac and relief for another Aussie bank. The fine would be the biggest corporate fine in Australian history. Westpac has revealed it expects the ongoing AUSTRAC investigation will cost it $1.03 billion. Such a fine will represent about 15% of the bank's 2019 profit. Shame: In November last year AUSTRAC, the entity responsible for preventing financial crimes, said the bank had violated anti-money laundering and counter-terrorism laws more than 23 million times (which the bank admits), allowing money tied to child exploitation in south-east Asia to flow freely. For example, Westpac's system was used by paedophiles to send money to the Philippines to pay for child abuse material without raising any red flags. Notwithstanding Westpac's admission, the bank is not going down without a fight. In the 57-page defence document filed with the court, Westpac denied AUSTRAC'S accusation that it failed to identify activity indicative of child exploitation risks. Leadership Failure: The scandal brought down Westpac's leadership, forcing the resignation of chief executive Brian Hartzer and the early retirement of chairman Lindsay Maxsted. Financial Pain: Last year Australian financial press reported that a penalty or settlement of $2 billion or $3 billion would see its CET1 ratio falling below 10.5% meaning the bank would be forced into another equity raising. And the trouble doesn't stop there for Westpac as the corporate regulator, ASIC, is probing into Westpac's previous $2.5 billion equity raise. Relief: Commonwealth Bank will be delighted to pass the mantle of the indignity of Australia's current money laundering record fine of $700 million to Westpac (Commonwealth Bank was fined for systemically failing to report around 54,000 suspicious transactions made through its "intelligent deposit machines"). If you want more on the story from the media, there are updates on an almost weekly basis - soon I guess daily basis. Just use this link to keep track of the story: "Westpac Austrac money laundering fine". And add case to your case studies and typologies in your AML / CTF training for everything from CDD, transaction monitoring, risk assessment, culture, condusct risk and (lack of) crisis management. Peter Oakes, Founder, CompliReg Peter Oakes is an experience anti-financial crime, fintech and board director professional. He served as Ireland's first Director of Enforcement and Financial Crime Supervision at the Central Bank of Ireland (2010-2013) in the aftermath of the financial crisis, leading the investigation and enforcement efforts into the Irish banking industry. Peter is a regular contributor to, and moderator and panel member at, ACAMS events.

Back to Blog

16 January 2020: Peter Oakes, Founder of CompliReg (and Founder of Fintech Ireland, Fintech UK, Fintech NI and US Fintech / USTechFin) has been recognised as a Leading Band 1 Consultant in Chambers & Partners’ 2020 Professional Advisers guide for FinTech – the premier ranking of professional advisers to the financial services industry.

Peter secured a nationwide Ireland Band 1 ranking – Chambers’ top-tier ranking – where it was noted that: Peter Oakes, who has vast international regulatory experience as a former director of the Central Bank of Ireland. A source says: ‘Peter is high-profile, he has very strong governance capabilities and is very good for a regulated FinTech company.' Peter is a non-executive director of regulated fintech companies in the payments, e-money and MiFID sectors and is an adviser and mentor to fintech and regtech startups and scaleups. In Ireland he is a consultant to Clark Hill and in the UK he is a consultant to Kerman & Co, which is supporting the Fintech UK project. Learn more about Peter Oakes’s rankings in the Chambers FinTech guide here: https://chambers.com/department/peter-oakes-consulting-fintech-49:2743:114:1:23173986

Back to Blog

"Perhaps they could be a company that's involved in lending and rather than you having to give your data in a form, you give them permission to scrape the detail from your account and they can say 'yep, we can see that that's your income, it's coming in every month and here's where your outgoings are'," said Peter Oakes, founder of FinTech Ireland.

There are currently just a handful of firms authorised by the Irish Central Bank to provide these kinds of added services, however many others that have approval from other European authorities will also be available here under 'passporting' rules. That means there may be many new functions available to online banking customers in the near future. "There's likely to be quite a demand for these sort of things from consumers," said Peter Oakes, founder of FinTech Ireland." https://www.rte.ie/news/business/2019/0913/1075730-open-banking-psd2/ |

© Peter Oakes (all rights reserved)

There is no consent nor legitimate interest right available to data vendors (e.g Zoominfo.com) and others to use email addresses, phone numbers and address details to send unsolicited marketing communications. This notice prevents you from claiming a business-to-business avenue to send unsolicited communications to any contact details appearing on this website. The email address PETER AT PETEROAKES.COM is a personal email address and is also protected by GDPR rights.

Privacy Statement.

There is no consent nor legitimate interest right available to data vendors (e.g Zoominfo.com) and others to use email addresses, phone numbers and address details to send unsolicited marketing communications. This notice prevents you from claiming a business-to-business avenue to send unsolicited communications to any contact details appearing on this website. The email address PETER AT PETEROAKES.COM is a personal email address and is also protected by GDPR rights.

Privacy Statement.